Technology & SaaS

SaaS: The Key Metric Your Start-up Should Be Measuring

Which SaaS metrics should you be measuring and Why? Our resident SaaS expert @Chris Short shares his thoughts

The ‘buy now pay later’ (BNPL) sector is growing at an incredible speed. The premise of BNPL is fairly simple. When customers reach an online checkout, they can choose to split their total bill into multiple instalments rather than paying the full cost up-front.

5 Buy-Now-Pay-Later start-ups who are changing the way we pay

The ‘buy now pay later’ (BNPL) sector is growing at an incredible speed.

The premise of BNPL is fairly simple. When customers reach an online checkout, they can choose to split their total bill into multiple instalments rather than paying the full cost up-front.

More and more businesses are now partnering with BNPL platforms to offer flexible credit to consumers. This payment system is also becoming commonplace in a diverse range of industries.

So what has caused BNPL to skyrocket in popularity?

The pandemic has played a major role. Consumers felt an enormous strain on their personal finances, particularly during the height of COVID - it’s easy to see why the flexibility of BNPL appealed to shoppers.

In fact, the use of BNPL servicesalmost quadrupled in the UK during the pandemic, with £2.7bn worth of transactions being completed by over 5 million customers.

Since BNPL is still a relatively new proposition in the world of FinTech, it’s largely unregulated, which explains the rapid growth of several different players in the market.

Although the UK Government have pledged to place more regulations on the industry, for the time being, BNPL platforms remain relatively unrestricted - meaning they’re free to continue expanding and evolving.

But which BNPL partners are currently leading the pack? We’ve identified 5 providers who are transforming the way that we pay.

Zilch

Zilch is one of the fastest-growing platforms in the market. This London-based startup has seen incredible success with its direct-to-consumer proposition.

The Zilch app allows users to spread their payments in any store where MasterCard is accepted, offering customers a compelling level of financial flexibility.

This direct-to-consumer focus means that Zilch has avoided time-consuming merchant acquisitions and integrations. Instead, they’ve carved out their own lane, achieving impressive growth as a result.

Zilch is currently valued at around $2bn and is backed by several high-profile investors, including Goldman Sachs. The fastest to reach unicorn status in Europe, Zilch has increased its customer base to over a million users in just 13 months!

That’s some serious momentum.

The platform is also continuing to innovate, having introduced BNPL to the gift-card market in Christmas 2021. By pushing their technology into new product areas, Zilch will undoubtedly continue to see consistent growth in the near future.

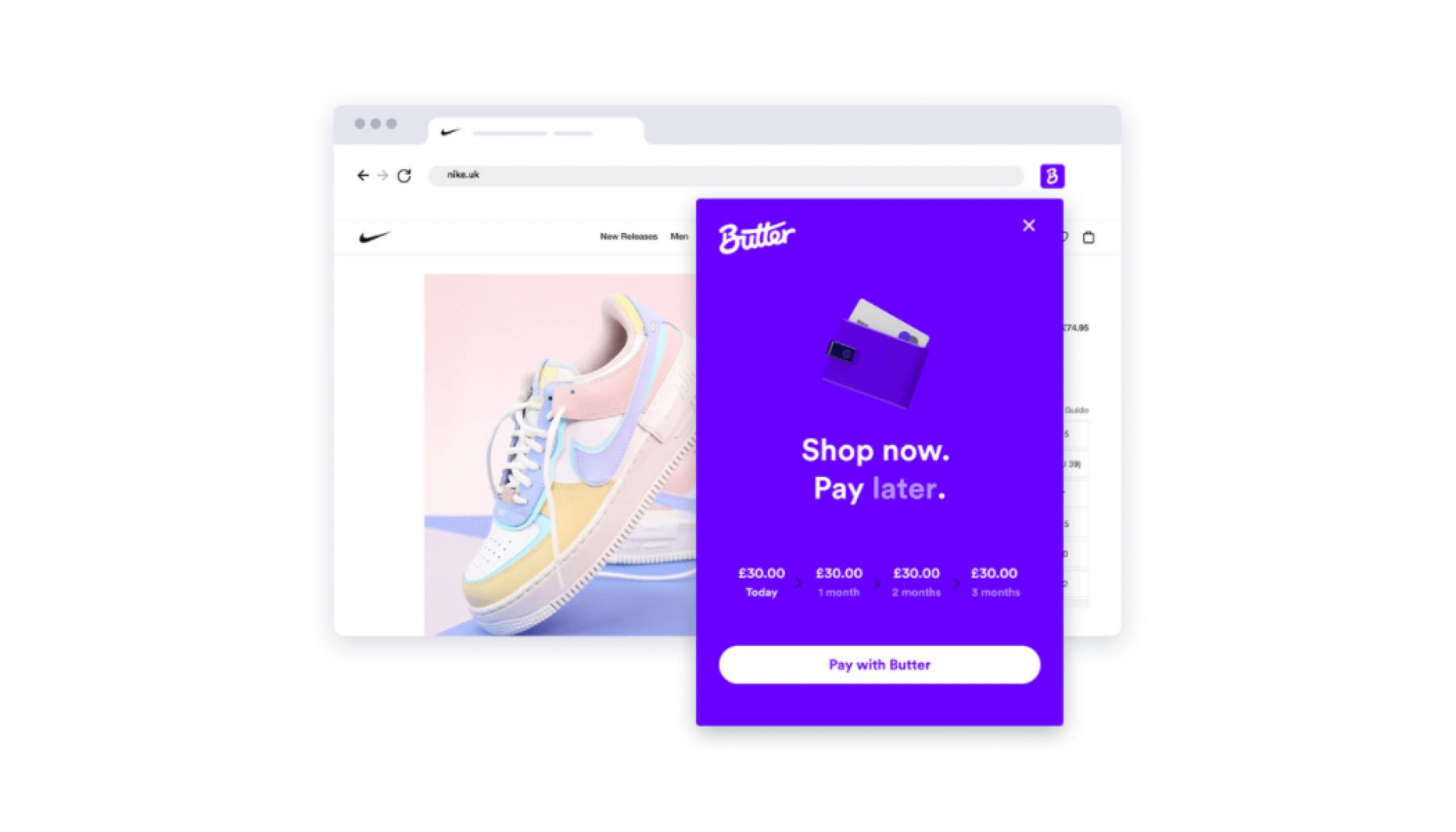

Butter

Butter introduced themselves to the BNPL sector with a unique proposition - simple repayments for the holiday industry.

There was a clear gap in the travel market for flexible payments, and Butter quickly established itself as a leading provider here. However, the global pandemic threw a fairly sizable spanner into the works, causing travel and tourism to effectively grind to a halt.

Butter reacted quickly to the COVID situation and expanded its BNPL offering beyond travel.

The app now enables customers to spread the cost of any online purchase, with adjustable repayment schedules and even a handy physical card available for users.

This emphasis on consumer accessibility has helped Butter to fuel significant growth - in 2021 the platform raised £15.8m in a round of investments. The agile move from travel to retail has proven to be a smart one for the platform, as its customer base has continued to grow.

Divido

Our fellow Camden-dweller Divido has been making a big impact in the BNPL market.

The platform brings a unique proposition to retail finance, acting as an intermediary between shoppers and credit lenders.

Lenders compete to offer consumers the most appropriate credit line at the point of sale, and Divido partners with various businesses (including banks, retailers and payment partners) to open up new lending opportunities.

This model allows Divido to offer higher acceptance rates and lower fees for consumers since the platform is working with multiple lenders. Plus, as credit suitability is reviewed by the lenders rather than Divido, the app is free to rapidly scale up and diversify.

Divido has already integrated with various established brands - including being appointed by Brompton Bicycle (Britain’s largest bicycle manufacturer) as a point-of-purchase partner in 2019.

A $15m Series A was closed in 2018, followed by a $30m Series B in 2021. Divido has its eyes on global expansion, and will no doubt use this funding to supercharge international growth.

Monzo Flex

Challenger banks like Monzo have already made massive strides in the FinTech sector - so it’s no surprise that Monzo has stepped into the world of BNPL finance with Monzo Flex.

With a banking customer base of around 5 million, Monzo is in a prime position to offer fluid repayments and introduced early access to Monzo Flex in September 2021.

Monzo Flex offers interest-free repayments over 3 instalments, plus easy adjustments and tweaks to repayment schedules. Plus, users can flex existing Monzo transactions (from up to 2 weeks prior) which provides customers with another convenient option for repayments.

The BNPL feature just requires an up-front application and pre-agreed credit limit, making it highly accessible to existing users.

Monzo has continued to go from strength to strength in recent times. The platform reached a valuation of $4.5bn in December 2021, shortly after receiving $500m in fresh investments.

Chinese tech giant Tencent has also joined the Monzo party, delivering a $100m top-up in the latest round of funding.

Equipped with serious financial momentum, a solid infrastructure and a pre-existing user base, Monzo is in a strong position to accelerate the growth of Monzo Flex.

DivideBuy

DivideBuy develops web-based software for e-commerce businesses and has looked to corner the market on credit lending for larger retail purchases.

The platform prides itself on total transparency and a lack of small print, which has proven to be a major selling point for new customers.

The app has already seen success with major retail partners, including e-commerce mattress brand Simba who reported a 25% increase in conversion rates while partnering with DivideBuy.

In more recent times the platform expertly navigated the COVID chaos, offering integrations with smaller retail businesses struggling with declining profits and slow recovery.

DivideBuy also offered flexible subscription payments for these small businesses - a smart move that not only helped the app to source new partners but also helped retailers drum up new business.

In 2020 DivideBuy ranked first place on Deloitte’s UK Technology Fast 50 list, which is a testament to their consistent success in the FinTech market. Having just secured a £300m lending facility in September 2021 and a growing consumer appetite for BNPL, the future is bright for DivideBuy.

The BNPL sector is currently one of the most innovative in FinTech.

All of these major players have carved out a unique space in the market by focusing on different consumer needs - from frictionless holiday repayments to credit for big-ticket purchases.

Although regulations in the industry will inevitably tighten, consumer interest in BNPL technology is clear. So expect to see more unique startups emerging in the near future!

If you would like to discuss hiring plans for your finance or operations teams, please get in touch at [email protected]

Which SaaS metrics should you be measuring and Why? Our resident SaaS expert @Chris Short shares his thoughts

In the past two decades we have seen exponential growth in the Tech start-up and scale-up space and there is one trait, regardless of industry or sector, whether in SaaS, Artificial Intelligence, Fintech, e-commerce, HealthTech, AdTech or a whole host of others, that they have in common and that is exponential headcount growth.

With the pandemic still raging in the US, 2021 was a difficult year for many. However, the year also saw a huge amount of growth in many tech sectors with no sign of slowing down.

When we work in harmony, great things happen. Let’s show you how.

Get the latest insights, tips, and opportunities straight to your inbox – sign up today!